“When your work speaks for itself, don’t interrupt.” [Henry J. Kaiser]

Abstract

If you need to generate correlated random numbers, the Iman Conover approach is a good method which is to be preferred to the Cholesky decomposition.

In 1982 Iman and Conover published their original article (external link!) “A distribution-free approach to inducing rank correlation among input variables”.

Rick Wicklin wrote in 2021 on (external link!) “Simulate correlated variables by using the Iman-Conover transformation”. His article includes a SAS implementation of the Iman Conover approach.

In 2005 Stephen J. Mildenhall published (external link!) “Correlation and Aggregate Loss Distributions with an Emphasis on the Iman-Conover Method”.

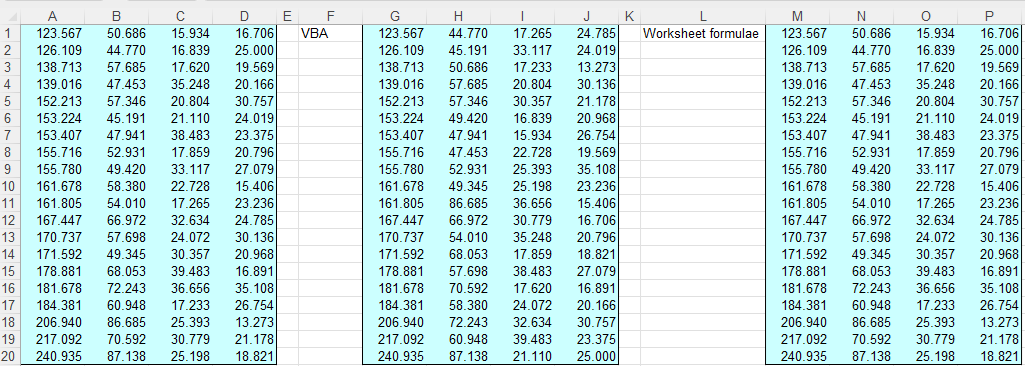

I implemented the example given in Mildenhall’s paper with Excel worksheet functions as well as with Excel / VBA:

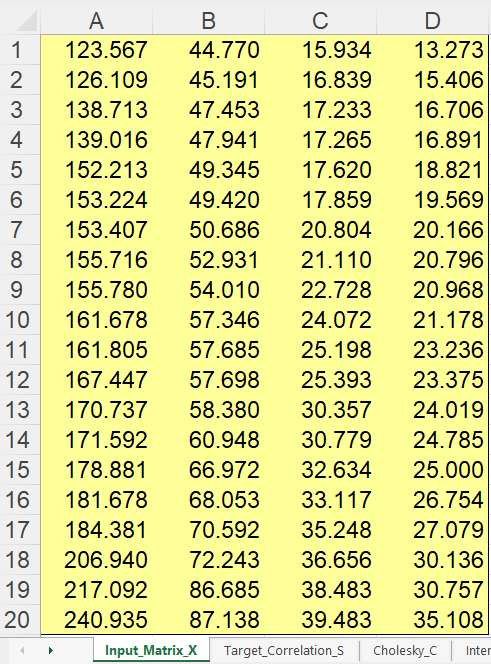

The input matrix X:

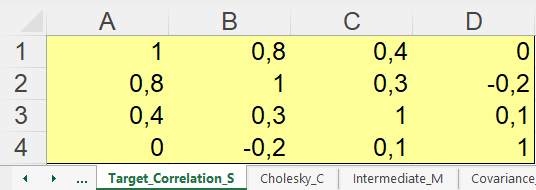

The target correlation S:

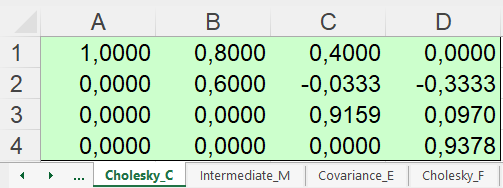

The Cholesky decomposition C of S:

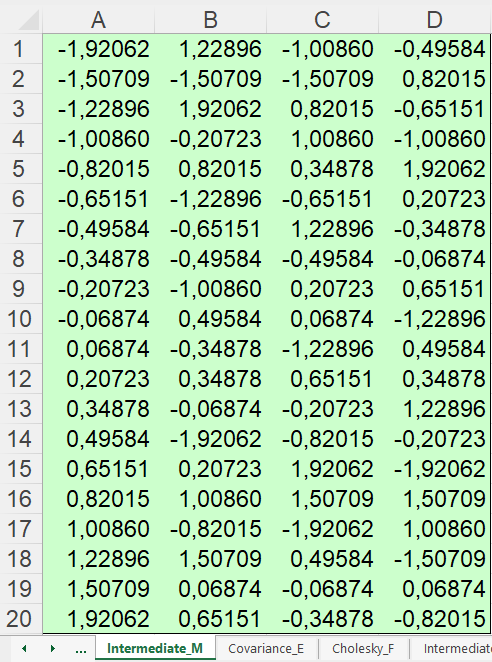

The intermediate matrix M (constant values to equal Mildenhall’s data):

You can create similar data automatically with an array formula in A1:A20:

=NORM.S.INV(SEQUENCE(20,1,1,1)/21)/STDEVPA(NORM.S.INV(SEQUENCE(20,1,1,1)/21))

or with the array formula

=TRANSPOSE(RandomShuffle($A$1:$A$20))

in cells B1:B20 (copy to columns C and D respectively).

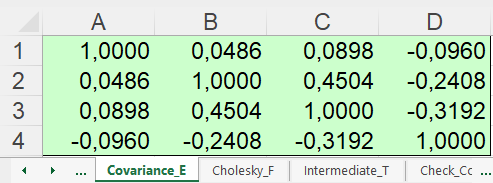

Now you get the covariance matrix E:

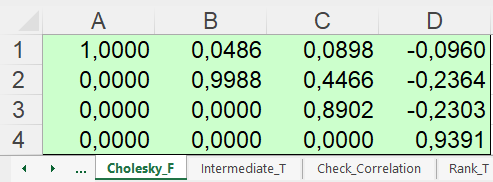

And its Cholesky decomposition F:

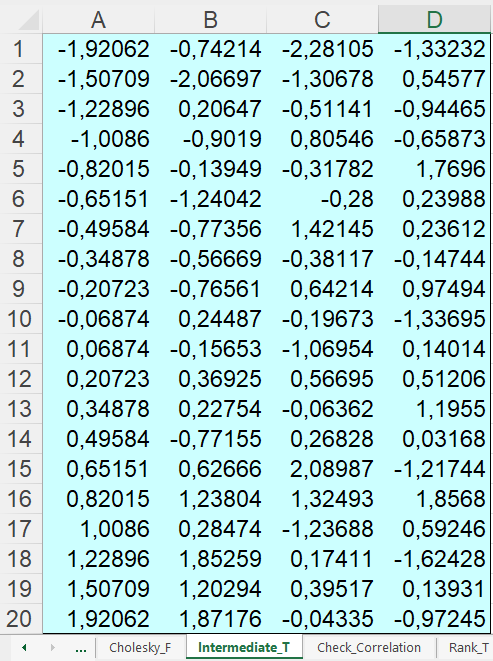

The intermediate matrix T:

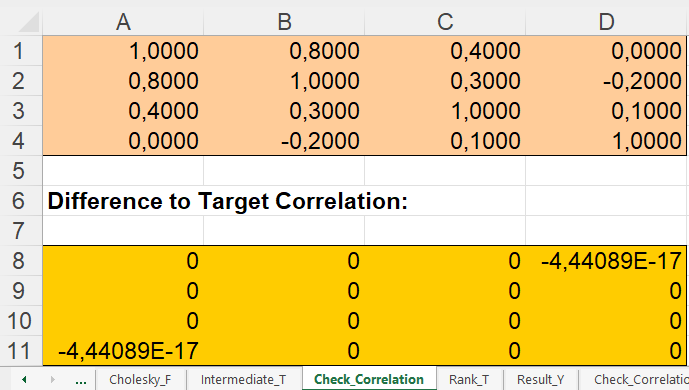

You can check the generated correlations:

Calculate the ranks of numbers in the columns of T in sheet Rank_T:

![]()

![]()

Finally you get your result in sheet Result_Y:

You can check the difference to the target correlation in sheet Check_Correlation_Result:

Appendix – IndexX Code

Please read my Disclaimer.

Function IndexX(n As Long, arr As Variant, colNo As Long) As Variant

'Indexes an array arr[1..n], i.e., outputs the array indx[1..n] such

'that arr[indx[j]] is in ascending order for j = 1, 2, . . . ,n. The

'input quantities n and arr are not changed. Translated from [31].

Const m As Long = 7

Const NSTACK As Long = 50

Dim i As Long, indxt As Long, ir As Long, itemp As Long, j As Long

Dim k As Long, l As Long

Dim jstack As Long, istack(1 To NSTACK) As Long

Dim a As Double

ir = n

l = 1

ReDim indx(1 To n) As Long

For j = 1 To n

indx(j) = j

Next j

Do While 1

If (ir - l < m) Then

For j = l + 1 To ir

indxt = indx(j)

a = arr(indxt, colNo)

For i = j - 1 To l Step -1

If (arr(indx(i), colNo) <= a) Then Exit For

indx(i + 1) = indx(i)

Next i

indx(i + 1) = indxt

Next j

If (jstack = 0) Then Exit Do

ir = istack(jstack)

jstack = jstack - 1

l = istack(jstack)

jstack = jstack - 1

Else

k = (l + ir) / 2

itemp = indx(k)

indx(k) = indx(l + 1)

indx(l + 1) = itemp

If (arr(indx(l), colNo) > arr(indx(ir), colNo)) Then

itemp = indx(l)

indx(l) = indx(ir)

indx(ir) = itemp

End If

If (arr(indx(l + 1), colNo) > arr(indx(ir), colNo)) Then

itemp = indx(l + 1)

indx(l + 1) = indx(ir)

indx(ir) = itemp

End If

If (arr(indx(l), colNo) > arr(indx(l + 1), colNo)) Then

itemp = indx(l)

indx(l) = indx(l + 1)

indx(l + 1) = itemp

End If

i = l + 1

j = ir

indxt = indx(l + 1)

a = arr(indxt, colNo)

Do While 1

Do

i = i + 1

Loop While (arr(indx(i), colNo) < a)

Do

j = j - 1

Loop While (arr(indx(j), colNo) > a)

If (j < i) Then Exit Do

itemp = indx(i)

indx(i) = indx(j)

indx(j) = itemp

Loop

indx(l + 1) = indx(j)

indx(j) = indxt

jstack = jstack + 2

If (jstack > NSTACK) Then

'STACK too small in indexx

IndexX = CVErr(xlErrNum)

Exit Function

End If

If (ir - i + 1 >= j - l) Then

istack(jstack) = ir

istack(jstack - 1) = i

ir = j - 1

Else

istack(jstack) = j - 1

istack(jstack - 1) = l

l = i

End If

End If

Loop

IndexX = indx

End Function

Appendix – RandomShuffle Code

Please read my Disclaimer.

Function RandomShuffle(vtemp As Variant) As Variant

Dim j As Long, k As Long, n As Long

Dim temp As Double, u As Double

'Application.Volatile 'Uncomment if you think you need this.

With Application.WorksheetFunction

On Error Resume Next 'Ignore error: VBA calls already with 1-dim array.

vtemp = .Transpose(vtemp)

On Error GoTo 0

n = UBound(vtemp)

j = n

Do While j > 0

u = Rnd()

k = Int(j * u + 1)

temp = vtemp(j)

vtemp(j) = vtemp(k)

vtemp(k) = temp

j = j - 1

Loop

RandomShuffle = vtemp

End With

End Function

Appendix – ImanConover Code

A VBA solution to generate correlated numbers with the Iman Conover approach is given here. I have included this code into my sbGenerateTestData application, too.

Please notice that the function ImanConover requires (calls) the functions

IndexX and RandomShuffle mentioned above as well as the function

Cholesky.

Please read my Disclaimer.

Function ImanConover(rInputMatrix As Range, _

rTargetCorrelation As Range) As Variant

'Implements the Iman-Conover method to generate random

'number vectors with a given correlation.

'Algorithm as described in:

'Mildenham, November 27, 2005

'Correlation and Aggregate Loss Distributions With An

'Emphasis On The Iman-Conover Method

'V0.3 PB 02-Nov-2024 by Bernd Plumhoff

Dim vX As Variant 'Input matrix

Dim vS As Variant 'Target correlation matrix

Dim vC As Variant 'Cholesky decomposition of vS

Dim vM As Variant 'Intermediate matrix M

Dim vE As Variant 'Covariance matrix E

Dim vF As Variant 'Cholesky decomposition of vE

Dim vT As Variant 'Intermediate matrix T

Dim d As Double, dS As Double

Dim i As Long, j As Long, k As Long

Dim lRow As Long, lCol As Long

Dim state As SystemState

With Application

Set state = New SystemState

vX = .Transpose(.Transpose(rInputMatrix))

lRow = rInputMatrix.Rows.Count

lCol = rInputMatrix.Columns.Count

'#############################################################################

'# Check inputs #

'#############################################################################

If lCol <> rTargetCorrelation.Columns.Count _

And rTargetCorrelation.Rows.Count <> rTargetCorrelation.Columns.Count Then

'Structure of target correlation matrix needs to fit input matrix

ImanConover = CVErr(xlErrNum)

Exit Function

End If

vS = .Transpose(.Transpose(rTargetCorrelation))

For i = 1 To lCol

If vS(i, i) <> 1# Then

'Target correlation matrix not 1 on diagonal

ImanConover = CVErr(xlErrValue)

Exit Function

End If

For j = 1 To i - 1

If vS(i, j) <> vS(j, i) Then

'Target correlation matrix not symmetric

ImanConover = CVErr(xlErrValue)

Exit Function

End If

Next j

Next i

vC = .Transpose(Cholesky(vS))

'#############################################################################

'# Create intermediate matrix M #

'#############################################################################

ReDim vMV(1 To lRow) As Double

d = 0#

dS = 0#

For i = 1 To Int(lRow / 2)

vMV(i) = .NormSInv(i / (lRow + 1))

vMV(lRow - i + 1) = -vMV(i)

d = d + 2# * vMV(i) * vMV(i)

Next i

If lRow Mod 2 = 1 Then vMV((lRow + 1) / 2) = 0 'Just for clarity, it's already 0

d = Sqr(d / lRow)

For i = 1 To lRow

vMV(i) = vMV(i) / d

Next i

vM = vX

For i = 1 To lRow

vM(i, 1) = vMV(i)

Next i

Dim vMW As Variant

For i = 2 To lCol

vMW = RandomShuffle(vMV)

For j = 1 To lRow

vM(j, i) = vMW(j)

Next j

Next i

'#############################################################################

'# Calculate covariance matrix E #

'#############################################################################

vE = vC

For i = 1 To lCol

vE(i, i) = .Covar(.Index(.Transpose(vM), i), .Index(.Transpose(vM), i))

For j = i + 1 To lCol

vE(i, j) = .Covar(.Index(.Transpose(vM), i), .Index(.Transpose(vM), j))

vE(j, i) = vE(i, j)

Next j

Next i

vF = .Transpose(Cholesky(vE))

vT = .MMult(.MMult(vM, .MInverse(vF)), vC)

'#############################################################################

'# Compute ranks of matrix T #

'#############################################################################

Dim vRT As Variant, vR As Variant

vRT = vX

For j = 1 To lCol

vR = IndexX(lRow, vT, j)

For i = 1 To lRow

vRT(i, j) = vR(i)

Next i

vR = IndexX(lRow, vX, j)

For i = 1 To lRow

vX(i, j) = vX(vR(i), j)

Next i

Next j

'#############################################################################

'# Calculate result matrix Y #

'#############################################################################

Dim vY As Variant

vY = vX

For i = 1 To lRow

For j = 1 To lCol

vY(i, j) = vX(vRT(i, j), j)

Next j

Next i

ImanConover = vY

End With

End Function

Download

Please read my Disclaimer.

mildenhall_example_on_iman_conover.xlsm [71 KB Excel file, open and use at your own risk]

Note: A comprehensive documentation of my Excel implementations can be found in Excel VBA A Collection.